Where your construction company’s money comes from, and where it goes is called cash flow. Cash flow is valuable information for all business owners, especially for construction businesses. An accurate cash flow projection gives you the knowledge to better predict your cash needs months in advance. In turn, this can help your construction business grow and show you when a problem is coming on the horizon. Cash flow can be a significant problem for construction companies. Understanding how cash moves through your business throughout the year is critical to success.

Cash flow is essentially your business’s wallet. It shows how much money you actually have on hand at a certain point in time. A cash flow statement is an analysis of all the cash that came in and went out for a given period (usually one month). When the period is in the future, the report is called a cash flow projection. Past reports are good to keep around because they can help you spot trends and predict future report amounts.

Cash flow projection for contractors: Predicting the future

There are two really good reasons to perform a cash flow projection – also called a forecast – for your construction company. First, it helps you predict cash shortfalls or surpluses in the coming months. If you know that your project sales always drop in December and January, you can make strategic moves to counter that tendency. Or, if you discover that the summer months are particularly profitable, you can get a sense of how much you need to set aside to save for the slow times.

The second reason to create a cash flow projection is that it allows you to estimate the effects of a change to your business. For example, if you decide to buy a new truck, you can add that to your cash flow projection each month and see how it affects the bottom line for the next six months to a year. You can also use this data to see how much your sales will have to increase to cover this or any added expense.

Cash is not profit

It can be easy to confuse cash flow and profit. Both show the difference between your income and expenses. In construction, however, with its multiple contract and billing structures, there isn’t always a direct link between income and expenses for a certain time period. Sometimes you bill in one month and incur expenses in a different month. If this is the case, you need to know how much to save to cover the expenses that come later in the project.

For example, if you bill your customers one-third of the contract every month, but you incur one-half of your expenses in the first month, you will find that the income from that job may not cover your expenses for that month. This is why it is important to look at how your construction projects are billed and how expenses come in – a cash flow projection. You can do this for individual construction jobs as well as your whole company. Then you’ll know the best billing strategy to use so you can comfortably cover your expenses each month.

How to make a cash flow projection

Many accounting software programs, like Quickbooks, will create current and past cash flow reports based on data already in the system, so don’t spend hours working on this until you see if yours does.

Here we’ll go through the sections of a simple cash flow projection report so you can understand where the numbers come from. (Just in case you need to put one together by hand.)

Download this sample cash flow projection in Excel to see how it works in practice, and input your own numbers.

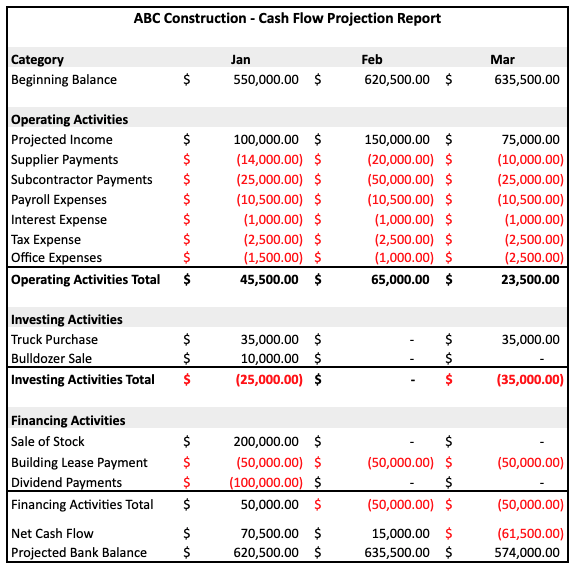

Note: Typically, an accounting spreadsheet uses parentheses to show a negative number. For example, ($10,000) is the same as -$10,000. A negative number will usually also be red. (Hence the expression “in the red,” which means you’re losing money.) Assume that a black number without parentheses is a positive amount.

A future cash flow projection report generally covers three types of cash activities:

- Operating activities

- Investing activities

- Financing activities

Operating activities include your income from sales, minus the cost of goods sold, labor expenses, and other costs of doing business. Investing activities include the purchase and sale of fixed assets (building, equipment, etc.). Financing activities include stock offerings and long-term debt. Your business may not be active in all three, so just report on the ones that apply.

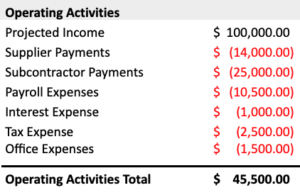

Operating activities

Net cash flow for operating activities is calculated this way:

- Take your projected total receipts from customers and other income.

Then, subtract: - Projected payments to suppliers, subcontractors, etc.

- Anticipated payroll expenses.

- Other projected business expenses not in other categories (licensing, interest, taxes, office supplies, etc.).

An example of operating activities:

- $100,000 potentially received from customers

- ($14,000) projected payments to suppliers

- ($25,000) payments to subcontractors

- ($10,500) payroll expenses

- ($5,000) other business expenses, interest, taxes

Projected cash flow from Operating Activities: $45,500.

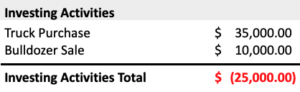

Investing activities

Cash flow from investing activities is shown by taking the amount of money planned to be spent during the period on purchasing fixed assets, and subtracting any income anticipated from the sale of similar assets.

Investing example:

Investing example:

- ($35,000) purchase of a new truck (negative because cash is going out)

- $10,000 income from sale of bulldozer

The sum results in a ($25,000) net negative cash flow (because we plan to spend more than we will take in)

Financing activities

Financing activities include things like issuing stock, payments on long-term debt, lease expenses, and payment of dividends. To report on these activities, you would add or subtract them to show money coming in or going out and provide a total for the section.

Financing example:

- $200,000 projected income from sale of stock

- ($50,000) building lease payment

- ($100,000) projected dividend payment to stockholders

The result is a $50,000 projected net positive cash flow.

When you take the total cash flow, positive or negative, from the three sections and add them together, you come up with the projected net cash flow for the period.

Here is how our example shakes out:

- $45,500 cash flow from operations

- ($25,000) cash flow from investing

- $50,000 cash flow from financing

That produces a $70,500 net positive cash flow for period.

Analyzing each of the categories on a regular basis will help you spot trends and see exactly where you are losing or making money.

Obviously, you don’t know exactly what your expenses and income will look like in the next 12 months, so all these figures are estimates. However, the best predictor of the future is the past! So use your actual cash flow from the last several months (or several years) to help you fill out a forecast for the future.

The real value to contractors: More cash in your pocket

An accurate cash flow forecast will help you know if you can pay your bills and when would be a good time to put some money away in savings. Without this type of analysis, your business could be floating along with no way to tell where it is heading or if there is a giant reef coming up. By taking a look into your company’s financial future, you can spot trends, predict shortages and surpluses, and see what the effect of a business change will be on your bottom line. Don’t underestimate the value of reviewing your past financial records to enlighten you on your future journey.